Marketing in Microfinance companies

CASE: RURAL BOXES

Through this interesting article we would like to share with you some of our experiences in the sector of financial companies, especially those that cover microfinance such as Rural Savings Banks. Here are a number of relevant points that we would like to take into consideration, in their current management as managers and directors, important points in the development and growth in local financial markets.

THE IMPORTANCE OF MARKETING IN LOCAL FINANCIAL INSTITUTIONS.

For our times, Marketing is of great importance because it has the responsibility of achieving productive growth, the income of every company, it must identify, evaluate and select market opportunities and establish strategies to acquire relevance and dominance in target markets. It proposes activities that aim to improve performance standards and efficiency of all managed resources. Marketing is developed in an integral way with all the areas of the organization and acts as a channel, as a protector of the company’s general strategy and as a way to conceive better and effective exchange relations. GHHH

The Rural Banks in the local financial markets.

In view of the competitive environment, the commercial orientation of some rural savings banks needs to be modified accordingly. There are several reasons (mostly shortcomings) for this comment:

- The low increase in new customers.

- The failure to cover and lead new markets, especially SMEs.

- The threat of competition. Especially Municipal Savings Banks, Edpymes as NGOs.

- There are no planned and different promotional campaigns.

- There is no persuasive and shocking advertising.

- There is no quality of service, it is a differentiating factor that creates a competitive advantage.

- An image of a financial entity only for the rural sector: agriculture, livestock, others.

Our firm ABC Marketing, has conducted several market studies, including some SWOTs in the Rural Boxes, and for the most part the most significant weakness (comments of staff) is the lack of importance of managers and directors to Marketing. There is no update in the commercial strategies, advertising and image of the savings banks, such as that of their financial products both active and passive, which in some cases are not attractive to the local market. Marketing is based on the diversification of the range of services, boosting it! Customer loyalty (the main objective of any company), is obtained from the satisfaction of their needs globally.

As is the case of Banco Mi Banco, which not only provides financial services, but also provides training, insurance, entertainment, promotions and a business exchange for its active clients. It has obtained leadership in the SME sector in Lima and is now in a stage of expansion into the provinces. The current management in the savings banks has been very passive (in the aspect of marketing) does not have the aggressiveness of the case to compete in markets increasingly invaded by non-local entities

Change of Business Mentality

This requires a change of perspective, a change of vision that leads some savings banks to become more competitive and take advantage of their advantages and benefits with a small and well-managed investment in marketing. Some financial institutions, such as Rural Savings Banks, perceive this as traditional commercial management, as they were in the past, with the mentality of “waiting for customers”, as if our institution were the only one, the most important and necessary for the local market.

Now times have changed and the customer-user is more demanding and has more alternatives to choose from. The Rural Savings Banks have many advantages that have not yet been fully exploited, they are entities with local capitals, of the region. Regionalism is one of the many competitive advantages they have.

- It focuses on selling the services requested by the client. Their response to the client’s requirements was punctual.

- The initiative started with the client who came to the entity in search of a specific service that would satisfy their specific financial need.

- All commercial efforts were focused on attracting the greatest number of customers, without paying attention to the customer base in the financial institution.

- Attention and service conditions were the same for all customers.

- It focuses on achieving a long-term relationship and for as many services as possible.

- Encourages cross sales (progressive sale of active and passive services) and a proactive attitude in sales.

- It focuses both on attracting and retaining customers, but with special attention is the latter objective.

- A positive discrimination is practiced, with advantages in attention, conditions, treatment, etc., towards the best clients of the entity.

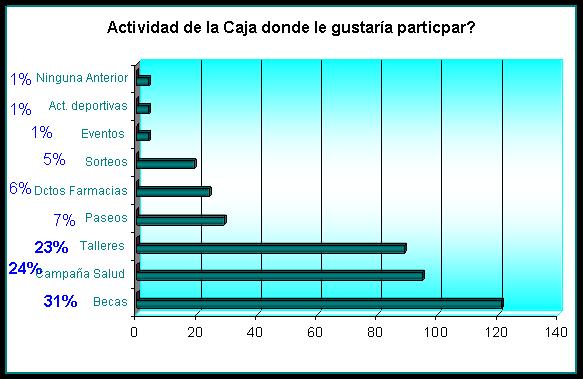

Marketing forces companies to go in search of the client, identifying the market needs (of the clients), planning actions that allow a greater commercial movement, a greater participation and a better positioning. Forming an organization that identifies itself in the market, especially the local population. Rural Savings Banks have an obligation to local authorities to lead preference through quality customer service, providing better services and covering more and more needs every day. In a study carried out in a savings bank, the population was asked what type of activities they would like to participate in, if any, if the savings bank improves its relations with its clients and not local clients.

In which activity of the Fund would you like to participate? 31% indicated that they would like to have Scholarships for their children, 24% participate in Health campaigns. 23% in training workshops. These data allow us to know that there are other hidden needs such as education for their children, health and personal training

Market share.

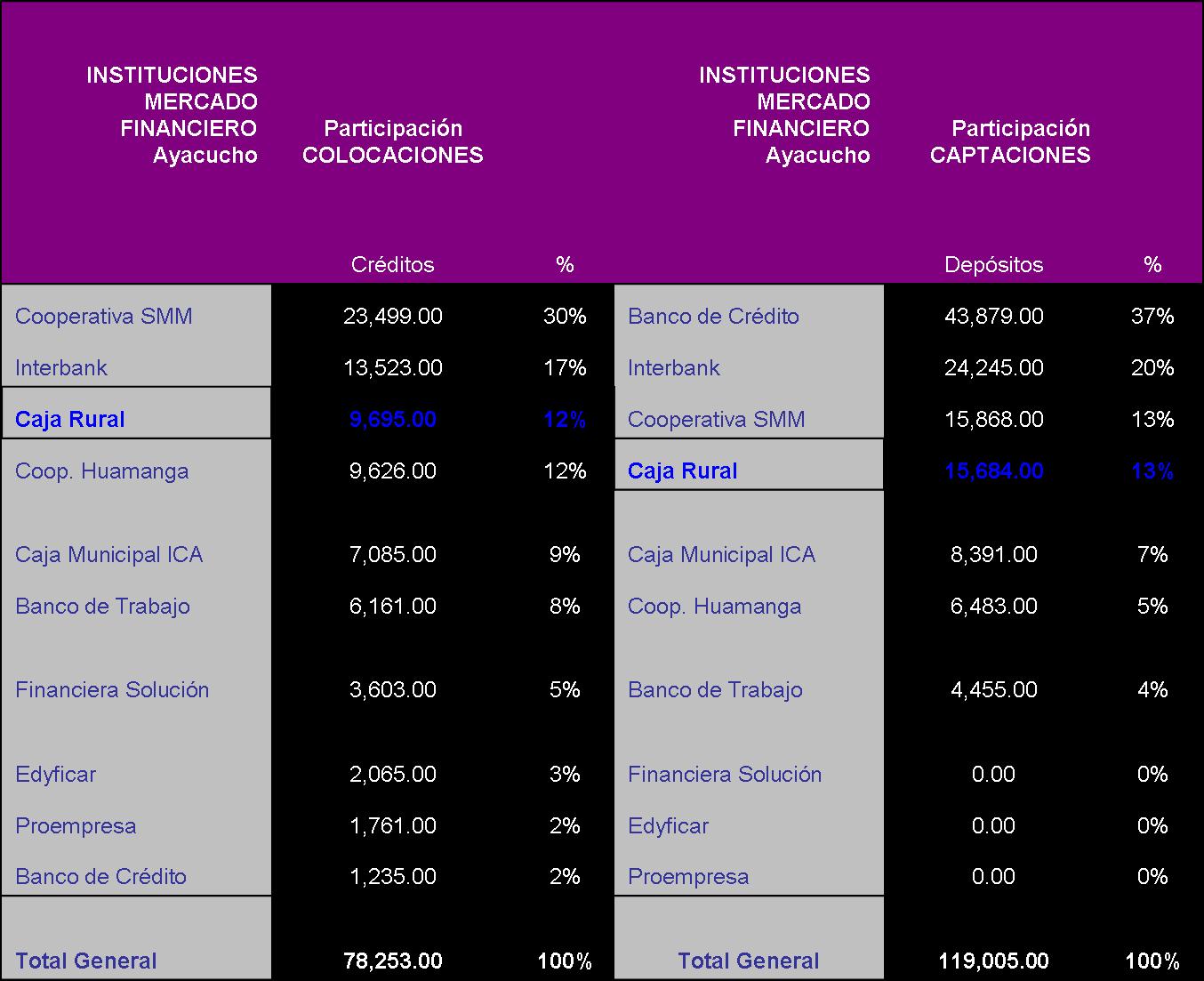

It is necessary to verify our market share in a certain period, to compare our objectives and the percentage achieved. Participation is a summary of our commercial activities compared to the competition. This is an indicator that allows us to determine our future goals. Marketing actions have a great influence on this aspect. Because through an action or strategy we can increase the percentages. As an example we have what happened in Ayacucho, where the Caja Rural carried out a Sweepstakes promotion, with very striking prizes (several cars) and obtained an increase in its participation in captures. Obtaining in the year 2003, the third place of the entities with greater captures, surpassing the 15 000, 000 of new soles The investment made was more than 100,000 new soles and was obtained captures greater than 5 000,0000 with regard to last year. The result is a very favorable cost/benefit for the Fund.

Positioning in the Market

In the opportunities we have had to work for a Caja Rural, the positioning has been one of the most important factors in the analysis. Positioning is more than the perception that the population has of our company. It is the reminder in the mind of the end user. But this point has many angles, one of them is that the population under study and even recognized by the same officials, the Caja Rurales, by their origins are related to the countryside, ie there is still the perception that they are entities that provide only credit to farmers, ranchers and all farm activity. In one of our visits to a province, a taxi driver was asked leaving the airport, if he knew any box (financial entity), and immediately responded the name of a Municipal Box. Tell me there is a local box, and the answer of several was that there was no local box. In other words, the Caja-Localidad relationship is null and void in many cases.

It is in this aspect that the rural cajas must make a turn, since the cajas cannot be limited by positioning an image of a financial entity for only one sector, but they should improve their image and their commitment to all segments of the local financial market. In two studies carried out both in Cajamarca and Ayacucho, the positioning or reminder of savings banks is very low in relation to other financial institutions. In some cases, the population was not aware of all the services provided by a savings bank. Another appreciation is the poor customer service provided by the staff of the savings bank.

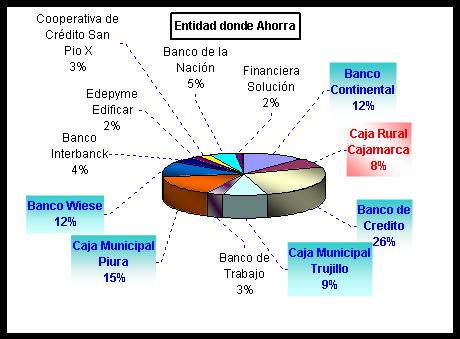

Question: In which institution do you prefer to deposit your savings? Source: ABC Marketing market study. City of Cajamarca: Interpretation: 25% of the population responded to the Banco de Crédito, this figure confirms leadership at the national level. However, this positioning has its other side in the population that is an entity for a certain segment (high A and B) and that is very safe, but the cost of maintenance and administrative expenses are high which implies that it is not profitable. In second place is Caja Piura, which has positioned itself strongly in Cajamarca without being a local entity, promotional campaigns with strong investment in trained personnel but the aggressive attitude in the market has allowed to lead in the non-banking sector. With 12% are Banco Wiese and Banco Continental, which target AB segments especially large companies such as Minera Yanacocha. With 9% Caja Trujillo, in a short time in the local market is gaining position as the fastest entity to provide credit. Caja Rural is with 8%, despite being a regional entity is not well positioned. Dissemination and promotion have been very scarce due to many factors such as leadership, the lack of aggressiveness of the commercial force and the lack of promotional tools and instruments.

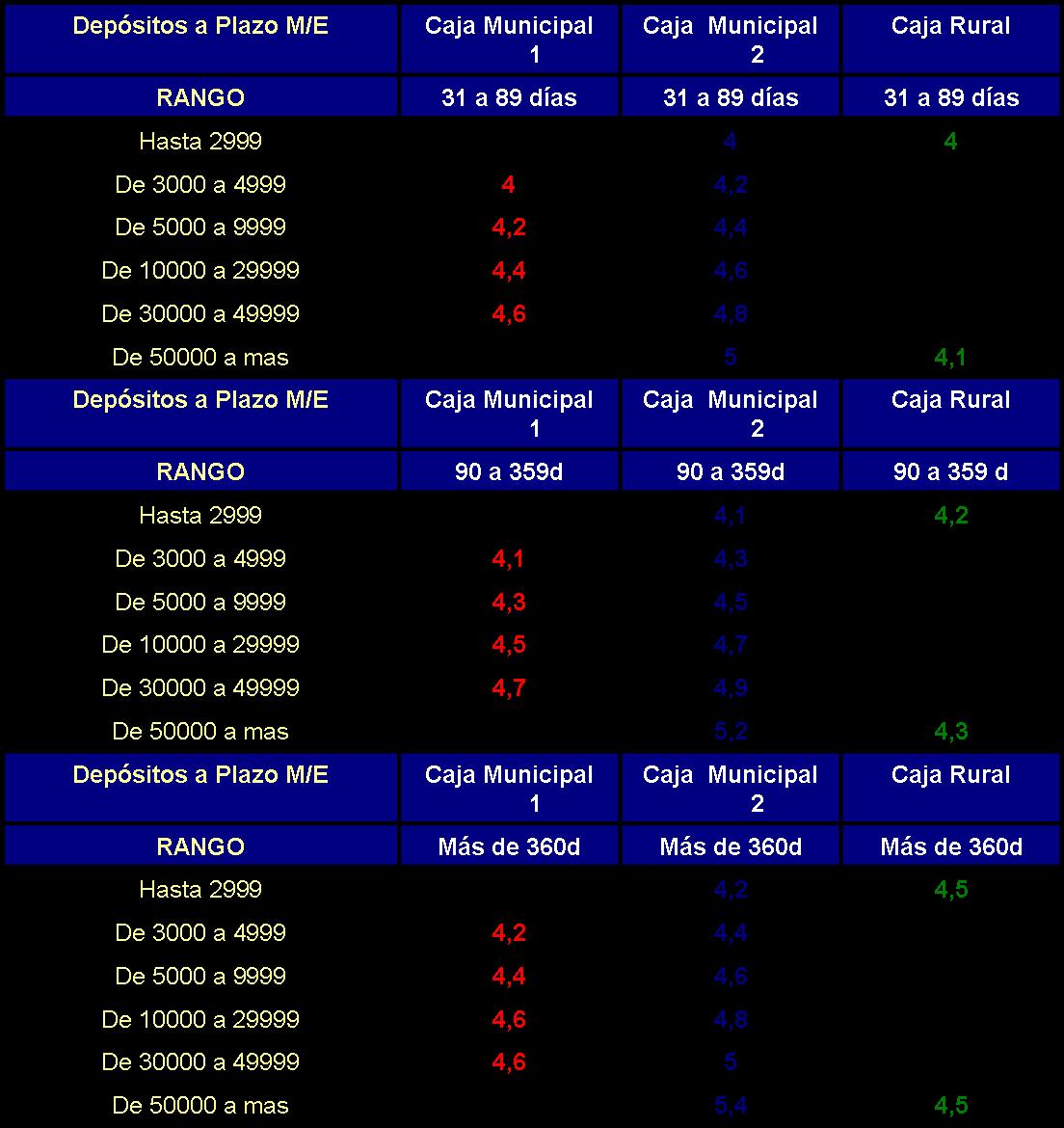

Variation in rates.

It is the result of simple market research, comparing rates in the market. In this case, working in one of the Rural Savings Banks, this type of table had rarely been carried out. In these cases, we can see that the rural savings bank’s rate policy is very different from those of its closest competitor in this case (example below) two municipal savings banks, which segment their rates according to the amount and also the time. These staggered rates allow them to differentiate their clients according to the amounts. The progressive form of the rates allows to cover more segments of markets that is to say more clients. in the example let’s suppose that a client wishes to deposit to Fixed Term a greater amount, the rural box will offer him the same rate that it gives to a deposit of smaller amount. On the other hand, in a municipal box it will offer you a higher and fair rate. These differences are only some that the market finds and that constantly the managers of the Rural Savings Banks must be to the expectation of these changes, to improve their offer to the market. Without a doubt, the rate is not a major factor in the final decision. But a good structure of rates, with good attention, good advertising and promotions, makes these big differences.

Quality of service.

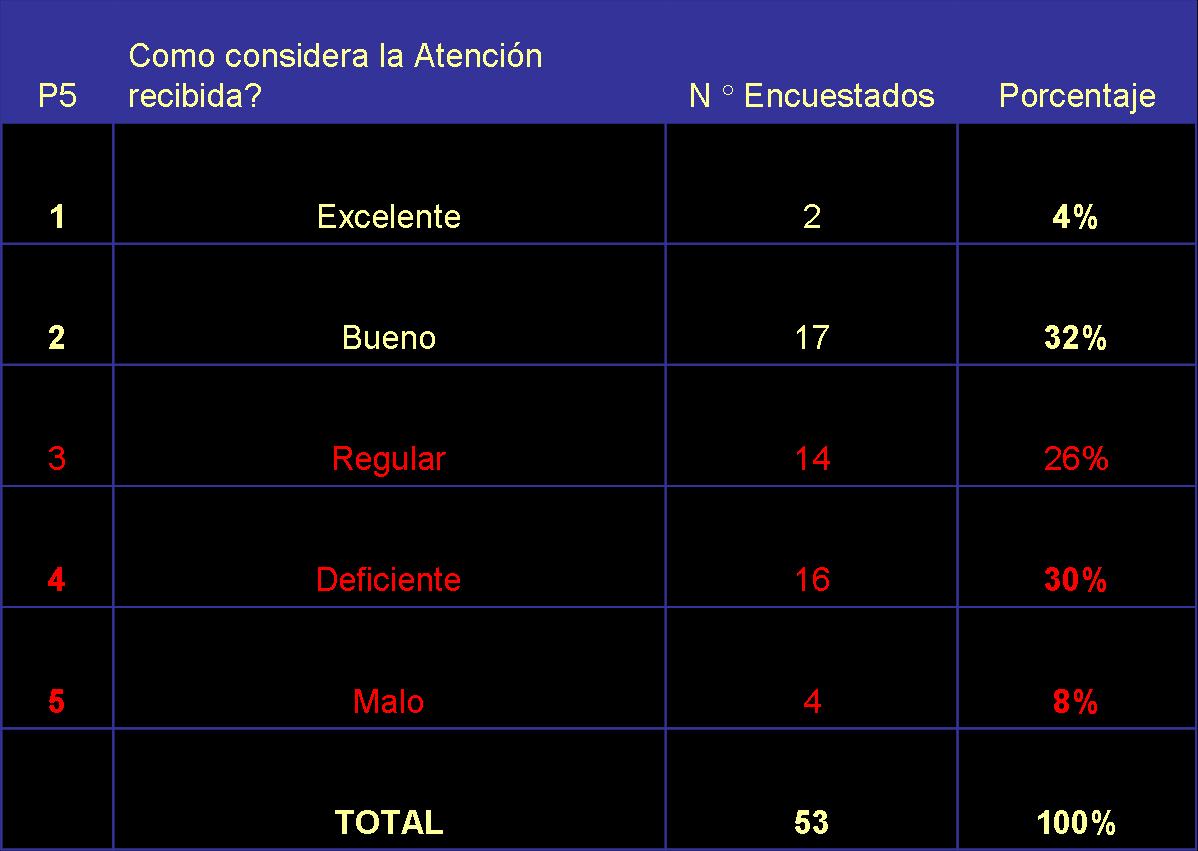

According to our experience in consulting and advising in some Rural Savings Banks, is the most negative factor in the Rural Savings Banks, still not perceived a solid culture of customer service. Many of these are poorly served and even discriminated against. There is not a good selection of personnel for the areas in contact with the client. In addition, there is a lack of training of personnel in sales techniques and human relations. it is always necessary to make an analysis and measure the degree of customer satisfaction. An average of 50 regular customers were surveyed in a rural client box. The purpose was to spontaneously perceive their comments about the degree of satisfaction, as well as the levels of quality in the attention and their suggestions about what they would like to receive from La Caja in the future.

Modification and increase of services.

Today, many financial institutions can offer the same product in the same market. According to the Marketing the ways of reaching the market, the way of selling can vary. Creativity here makes the difference in companies. The schemes have changed is for this reason that it is necessary to work on the modification of services. Highlighting the advantages and benefits provided by a service or product. It is also necessary to change the manuals and reduce procedures, to serve the customer faster and make it easy to use. Marketing can also detect new market niches and create services according to the needs of this. For example, we have the “Rapidiario” credit of the SMM Cooperative of Ayacucho, which offers this credit to merchants in the supply markets and they can pay daily installments, making this an accessible product with rapid capital mobility.

Change of advertising. Image of the boxes.

The images combined with movement, modern colors such as the type of letters and visual order are the great allies to obtain a mental positioning in people. Advertising over time with the help of technology has varied greatly. Boxes should constantly surprise their customers, the market. In 2004, we had the opportunity to be hired by an NGO, dedicated to providing loans for the construction of housing in less favored sectors. Their publicity was this only term, their name PROGRESO. Its publicity was this term with photos of the houses of the clients that had been built with this credit. Its objective was to cover more market. A total modification was necessary.

RECOMMENDATIONS.

To finalize our comments related to Marketing in the Rural Savings Banks, it is necessary to highlight the importance of the Savings Banks, for the development and growth of the regions. Currently, they are very interesting alternatives for customers-users, the low deposit rates, such as their high loan rates plus the high administrative expenses of the Banks, which led many customer segments to flee each day. To cite a case in the province of Chota, Cajamarca the Banco de Credito closed its branch, due to the rejection of the population. We have to consider that the provinces are in a growth stage, that they deserve a good service and above all the necessary conditions and the trust of entities according to their needs and reality. In that sense, the management of the Rural Savings Banks must be different in these times, worrying every day for the clients. Renewing and creating new ways to retain customers. There is a lot of work to be done, within this the Marketing can not be left to one side. Therefore it is necessary to invest consciously and prudently in Marketing to achieve the objectives set and desired by the managers.

Juan Carlos Maldonado

Marketing Consultant

ABC Marketing. Advice and Consultancy

{kind=link}